The Federal Reserve hinted that the current rate hike cycle is about to end, which sent the dollar tumbling to a nine-month low and Treasury yields to a decline.

The European Central Bank and the Bank of England are trying to catch up by increasing their key rates. After the closing, Apple, Amazon, and Alphabet release their financial results.

Oil prices plummet to a three-week low as a further significant increase in U.S. inventories implies a decline in demand.

Here are the financial market essentials for this week.

FOMC Press Statement on Rate Hike

The Fed increased rates as predicted by 0.25% to 4.75%, the highest rate of any major currency, in its FOMC Statement and Federal Funds Rate announcement.

This was their eighth straight rate increase. The FOMC Statement kept the same language indicating “ongoing” rate increases in the foreseeable future.

The committee kept its promise of “ongoing rate rises,” which appears to reinforce the dot plot’s intentions to raise rates by an extra quarter point in both March and May.

Powell effectively confirmed it as the current goal during his press conference when he said it would take “a couple more” hikes to reach an adequately restrictive policy.

Powell nonetheless asserted that the committee could now definitively state that the disinflationary process had begun.

According to the chair, supply-chain improvements are assisting the manufacturing sector, and new leases suggest that housing inflation will eventually improve.

Powell noted that he was more interested in long-term trends and was strikingly disinterested in the recent easing of financial conditions.

He stated that the market’s price of the Fed’s rate path primarily reflects the market’s expectation that inflation will decline more quickly than he expects.

He did not object to this. He also sounded upbeat about the prospects for a smooth landing and a persistently strong job market.

The Dollar, Treasury Yields Fall

Although Jerome Powell stated nothing particularly dovish during his press conference, his words had the effect of causing a robust bullish surge in equities and a selloff in the US Dollar.

The US Dollar and stocks initially hardly responded. Despite the possibility of additional rate increases, markets are pricing in none and, in fact, anticipate a 0.5% reduction in rates during the second half of 2023.

Although Chair Jerome Powell continued to say it would be “premature” to declare victory against inflation, he did recognize that a “disinflationary trend” has begun.

The Fed increased the target range for fed funds by 25 basis points to 4.50%-4.75%.

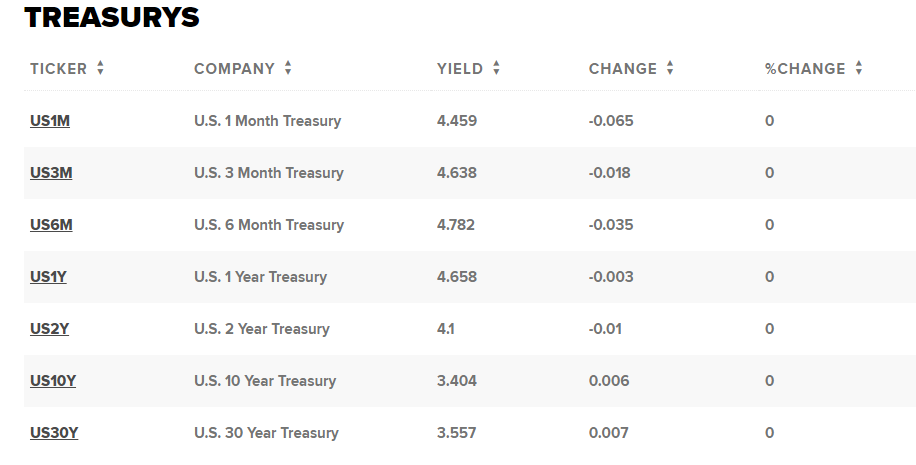

Before raising the rate, the dollar index reached a low of 100.675, while the yield on the two-year Treasury note dropped as low as 4.09%. But unlike the dollar, 2-year rates didn’t hit a new low.

Investor attention is currently on the Friday deadline for the January jobs data.

According to FactSet, economists forecast a fall from the 223,000 jobs added in December to an increase of 185,000 positions in January. The predicted increase in the unemployment rate from 3.5% to 3.6% is.

ECB Hikes Key Rate by 50 bps

The European Central Bank confirmed Thursday that its key interest rate would increase by 50 basis points to 2.5%.

It promised in a statement to “keep the course in raising interest rates significantly at a steady pace” and said it planned to raise rates by an additional 50 basis points in March, using unusually forceful language.

It claimed that keeping rates low would prevent price increases by reducing demand. It was noted that future meetings’ decisions would be based on the data.

The news caused markets to jump 1.3% on the day, seemingly indicating that the end of rate increases was near.

The action comes after four increases in 2022, which for the first time since 2014, lifted interest rates in the eurozone out of the negative territory.

According to preliminary data released on Wednesday, inflation in the eurozone decreased in January for the third consecutive month, but headline inflation remained high at 8.5%.

Energy and food are not included in core inflation, which was constant at 5.2%.

In a news conference held after the announcement, ECB President Christine Lagarde stated that “price pressures remain significant, in part because high energy costs are spreading throughout the economy.”

When discussing the economic situation in the eurozone, she pointed out that growth had slowed to 0.1% in the fourth quarter and was forecast to remain sluggish in the near future due to ongoing geopolitical unrest and more restrictive financing conditions.

She continued, “The risks to the forecast for economic growth have become more balanced,” pointing out that consumer confidence was rising, gas supplies were more secure, supply pressures were lessening, and rising wages and decreasing energy prices would encourage consumption.

She added that the economy has shown to be more resilient than expected and should continue to strengthen during the next quarters.

BoE Rises Key Rates To 4%

Despite raising interest rates by 0.5 percentage points to a 15-year high of 4%, the Bank of England suggested they may have peaked.

The BoE stated that more increases would only be required if there were fresh indications that inflation was going to stay excessively high for an extended period of time.

The BoE is now forecasting a milder recession this year than originally predicted.

The BoE’s current projections of decreasing inflation, according to Samuel Tombs, chief UK economist at Pantheon Macroeconomics, indicate that it “doesn’t intend to boost rates any further.”

Despite governor Andrew Bailey’s warning that the BoE still needed to be certain that inflation had been defeated, the bank abandoned its prior recommendation that it would need to act “forcefully.”

The Monetary Policy Committee increased rates for the tenth consecutive time by a vote of seven to two, one day after the US Federal Reserve raised rates by a quarter point and soon before the European Central Bank raised rates by 0.5 points.

Although the ECB stated that it would “keep the course” on rate increases, the BoE’s statement’s phrasing suggests that interest rates may peak at the new rate of 4%, which is lower than the 4.5 percent that financial markets were expecting.

The MPC stated that additional monetary policy tightening would be necessary “if there were evidence of more persistent [inflationary] pressures.”

On Thursday, the pound declined, falling 0.45% against the euro to €1.12 and 0.36 against the dollar to $1.23.

As the rate increased, the yield on the 10-year gilt decreased by 0.13 percentage points to 3.17 percent. The FTSE 100 in London was up 0.5% shortly after noon.

The BoE did not attempt to imply that the financial markets were mistaken to predict interest rate reductions later this year.

“The risks to inflation are weighted strongly to the upside,” the MPC members said.

According to the BoE’s latest central inflation prediction, price increases will soon slow from their December annual pace of 10.5% to less than 4% by the end of the year.

The BoE’s goal inflation rate of 2% is predicted to be significantly below in 2024.

In comparison to earlier estimates in November, the BoE’s predictions were less negative.

It anticipates that wholesale gas costs will be lower and businesses will be hesitant to lay off workers while the economy struggles.

Although the central bank now expects a slight recession, it clearly expected the UK economy to perform poorly for some time.

It expects the fourth quarter’s gross domestic product to fall 0.7% from the same period in 2022.

That is a little more pessimistic than the IMF’s prediction, which said last week that the UK GDP would contract by 0.5% over the same time.

BoE policymakers believe that the UK economy can only grow at a 1% annual rate if it creates inflationary pressures due to the likely supply of workers, limited business investment, and trade difficulties.

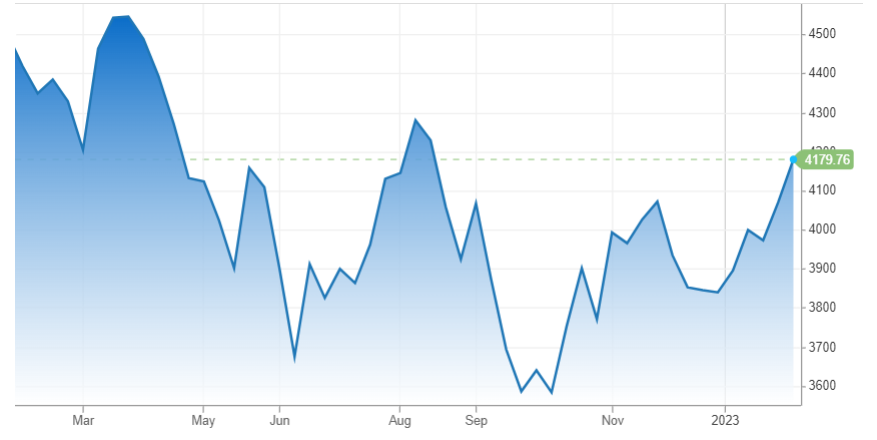

S&P 500, Nasdaq Hit Months Highest As Tech Stocks Rally

On Thursday, the S&P 500 reached its highest point in five months as better-than-expected Meta results further boosted confidence in technology shares, which had been the market’s biggest drag last year.

S&P 500 1yr

The broad market index increased by 0.8%, reaching its highest point since August. The tech-heavy Nasdaq Composite rose 2.4% to reach its highest point since September in the meanwhile.

The gains occur before three Big Tech earnings from Apple, Amazon, and Alphabet that will be released after the bell.

The Dow Jones Industrial Average underperformed at the same time, dropping 218 points, or around 0.6%.

Merck shares, which the pharmaceutical company offered a negative forecast for in its most recent quarterly results despite exceeding estimates on the top and bottom lines, pulled the main index lower.

After announcing a $40 billion stock repurchase and reporting a fourth-quarter revenue beat, Meta soared more than 24% on its highest day since 2013.

That made it easier for investors to overlook the metaverse business unit’s losses.

On the strength of those results, several mega-cap tech stocks increased. Alphabet, the company that owns Google, saw its shares rise by more than 5%, while Amazon saw a more than 6% increase.

Apple stock increased by more than 2%.

Boosted by recent indications of easing inflation, which investors anticipate may result in a slowdown in the Federal Reserve’s aggressive rate-hiking campaign, tech companies have risen in 2023.

After falling by more than 28% last year, the S&P 500 information technology sector is up more than 13% this year.

Oil Hits Three-Week Low

The U.S. government verified a significant increase in stockpiles last week, confirming a deteriorating demand among the world’s largest consumer and putting more downward pressure on crude oil prices.

For the fourth week in a row, gasoline stocks, a reliable indication of final demand, increased more than expected.

The quantity of U.S. commercial crude inventories is currently 3% higher than the five-year average and is the largest since June 2021.

By 05:55 ET on Thursday, Brent crude oil was down 0.1% at $82.75 a barrel, and U.S. crude futures had only recovered 0.1% from overnight lows to stand at $76.47 a barrel.

Both contracts were close to their lowest levels in three weeks.

Disclaimer:

All information has been prepared by TraderFactor or partners. The information does not contain a record of TraderFactor or partner’s prices or an offer of or solicitation for a transaction in any financial instrument. No representation or warranty is given as to the accuracy or completeness of this information. Any material provided does not have regard to the specific investment objective and financial situation of any person who may read it. Past performance is not a reliable indicator of future performance.